CCFS-2026 Extended to 31 August 2026: MCA Deadline

The Ministry of Corporate Affairs (MCA) has extended the Companies Compliance Facilitation Scheme, 2026 (CCFS-2026) to 31 August 2026. The earlier deadline of 15 July 2026 now moves to 31 August 2026, giving companies more working days to clear pending ROC filings at only 10% of the additional fees. The extension was granted through MCA General Circular No. 03/2026 dated 8 July 2026.

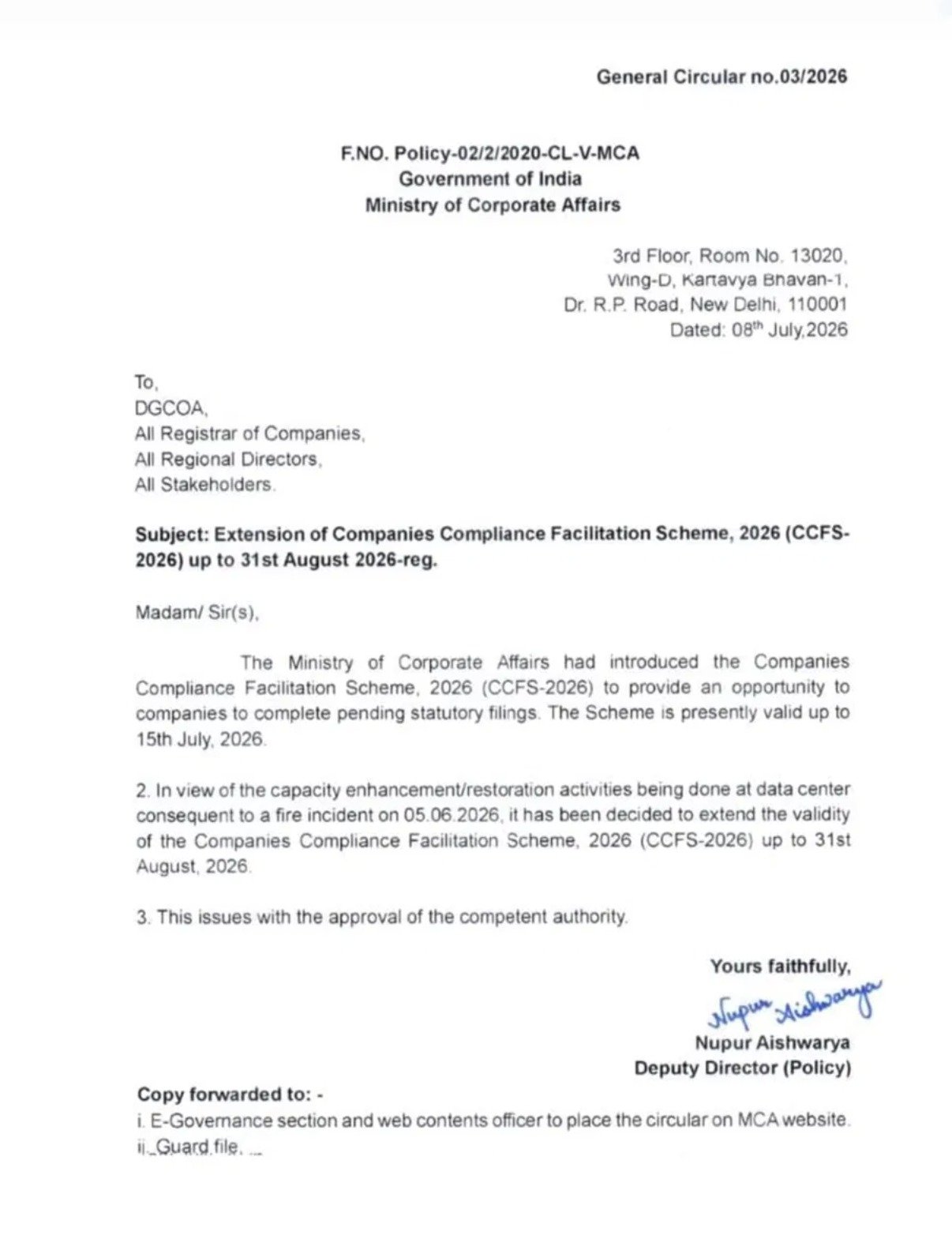

- CCFS-2026 is now valid up to 31 August 2026, extended from 15 July 2026 by MCA General Circular No. 03/2026 dated 8 July 2026.

- The extension follows data centre capacity and restoration work after the fire incident on 5 June 2026.

- Companies can clear pending annual filings by paying the normal fee plus only 10% of additional fees (a 90% reduction).

- Inactive companies can opt for dormant status (Form MSC-1) at 50% of the normal fee, or strike off (Form STK-2) at 25%.

- After 31 August 2026, full additional fees, adjudication notices and strike-off proceedings resume.

What has changed for CCFS-2026?

Only the deadline has changed. CCFS-2026 now runs up to 31 August 2026 instead of 15 July 2026, while the fee concessions, covered forms and eligibility conditions stay the same. The MCA confirmed this single change through General Circular No. 03/2026 dated 8 July 2026, issued from Kartavya Bhavan-1, New Delhi.

The scheme was introduced earlier by General Circular No. 01/2026 dated 24 February 2026 and was originally operative from 15 April 2026 to 15 July 2026. The extension does not add new forms or change the 10% additional-fee structure; it gives defaulting companies a longer window to file.

CCFS-2026 defined: The Companies Compliance Facilitation Scheme, 2026 is a one-time compliance relief scheme that allows companies to regularise overdue ROC filings at reduced additional fees. It is governed by Section 460 read with Section 403 of the Companies Act, 2013.

Why has MCA extended CCFS-2026 to 31 August 2026?

The MCA extended CCFS-2026 because of capacity enhancement and restoration work at its data centre following a fire incident on 5 June 2026. The incident disrupted MCA21 services during a peak filing period, so the regulator moved the deadline to 31 August 2026 to make sure companies were not penalised for a system-side disruption.

According to the circular, the extension issues with the approval of the competent authority and applies to all Registrars of Companies, Regional Directors and stakeholders. Companies that could not complete filings while MCA21 services were affected now get additional working days to finish.

The same fire incident triggered other emergency reliefs from the MCA around mid-2026, including extended timelines for certain e-form resubmissions and name reservations. The CCFS-2026 extension to 31 August 2026 is part of this wider set of accommodations for the MCA21 outage.

What are the revised CCFS-2026 dates?

CCFS-2026 opened on 15 April 2026 and, after the extension, closes on 31 August 2026. The table below sets out the key dates and the circulars behind them so you can track the timeline at a glance.

| Event | Date | Reference |

|---|---|---|

| Scheme notified | 24 February 2026 | General Circular No. 01/2026 |

| Scheme commencement | 15 April 2026 | General Circular No. 01/2026 |

| MCA data centre fire incident | 5 June 2026 | Cited in No. 03/2026 |

| Original end date | 15 July 2026 | General Circular No. 01/2026 |

| Extended end date | 31 August 2026 | General Circular No. 03/2026 |

What are your three options under CCFS-2026?

CCFS-2026 gives a defaulting company three routes: complete pending annual filings at reduced fees, become a dormant company, or strike off entirely. Each option has its own form and concessional fee, summarised below. Choose the route that matches whether the company will keep operating, pause, or close.

Option 1: Complete pending annual filings

Active companies that fell behind can file all overdue forms by paying the normal fee plus only 10% of the applicable additional fees. This clears the backlog and restores the company compliance status for its ROC annual filing obligations. It is the most common route for companies that intend to continue trading.

Option 2: Apply for dormant status

Dormant company defined: A dormant company is one that has no significant accounting transaction and is kept on the register for a future project or to hold an asset. Under Section 455 of the Companies Act, 2013, it files Form MSC-1 to obtain dormant status. Under CCFS-2026, the MSC-1 fee is 50% of the normal fee.

Option 3: Strike off the company

Strike-off defined: Strike-off is the removal of a company name from the Register of Companies, effectively closing it. It is filed on Form STK-2 with the ROC under Section 248 of the Companies Act, 2013. Under CCFS-2026, the STK-2 fee is 25% of the normal fee, which suits defunct companies with no ongoing operations. We assist with closure of a private limited company and business closure across entity types.

| Option | Form | Fee under CCFS-2026 | Governing Section |

|---|---|---|---|

| Clear pending annual filings | MGT-7, AOC-4 series, etc. | Normal fee plus 10% of additional fee | Section 403 |

| Dormant status | MSC-1 | 50% of normal fee | Section 455 |

| Strike-off (closure) | STK-2 | 25% of normal fee | Section 248 |

The percentages above (10%, 50% and 25%) are the concessional statutory fees payable to the MCA under CCFS-2026, calculated on the normal fees prescribed by the Companies (Registration Offices and Fees) Rules, 2014. Any IncorpX professional charges for end-to-end assistance are separate. Government / statutory fees are charged separately at actuals.

Which ROC forms are covered under CCFS-2026?

CCFS-2026 covers the standard set of overdue annual filing forms that attract additional fees. The main forms are:

- MGT-7 / MGT-7A: the annual return of a company (MGT-7A is the abridged form for small companies and one person companies).

- AOC-4 series: filing of financial statements, including AOC-4 XBRL and AOC-4 CFS for consolidated statements.

- ADT-1: notice to the ROC of appointment of an auditor. We assist with ADT-1 filing where this is pending.

- FC-3 and FC-4: annual accounts and annual return of a foreign company.

- Corresponding forms under the Companies Act, 1956 for older defaults.

Additional fee defined: An additional fee is the late fee charged over and above the normal filing fee when an e-form is filed after its due date. For AOC-4 and MGT-7, this is ₹100 per day per form since 1 July 2018, with no maximum cap.

How to file pending returns under CCFS-2026

Filing under CCFS-2026 follows the normal MCA process; only the fee is reduced. Complete these steps well before 31 August 2026, since last-minute filings often get rejected and corrections take time. Before you start, estimate the normal fees with our MCA fee calculator.

- Log in to the MCA portal and pull your company filing history to identify every pending form.

- Prepare the underlying documents: audited financial statements, board and audit reports, and director approvals for each defaulting year.

- Reconcile older defaults, as it is common to find missed forms from earlier years while preparing the annual return.

- File the overdue e-forms in the correct sequence (financial statements before the annual return for a given year).

- Pay the normal fee plus 10% of the additional fee at the time of filing, and save the challan and SRN for your records.

- Confirm the status of each SRN on the portal to make sure every form is taken on record.

In our experience assisting with these filings, the most common delay comes from missing prior-year forms that surface only when the latest annual return is prepared. Reconcile the full filing history first, then file year by year from the oldest default, so the sequence and fee calculation stay correct.

What immunity does CCFS-2026 offer?

CCFS-2026 offers conditional immunity from penalties, not blanket protection. For annual returns and financial statements under Sections 92 and 137 of the Companies Act, 2013, no penalty applies if the filing is completed before an adjudication notice is issued or within 30 days of receiving one. Beyond that, the penalty liability continues.

For other e-forms such as ADT-1 and FC-3, immunity from future penalties applies only where no prosecution or adjudication notice was issued before filing under the scheme. This is why filing early, rather than waiting for the deadline, protects the immunity itself.

What happens if you miss the 31 August 2026 deadline?

If you miss 31 August 2026, normal MCA rules resume in full. The additional fee reverts to ₹100 per day per form for AOC-4 and MGT-7 with no cap, and the ROC can issue adjudication notices and start strike-off proceedings. Companies with three consecutive years of non-filing also face director disqualification under Section 164(2).

Section 164(2) defined: Section 164(2) of the Companies Act, 2013 disqualifies a director of a company that has not filed financial statements or annual returns for three consecutive financial years. A disqualified director cannot be reappointed or appointed to any company for five years.

CCFS-2026 is time-bound and will not stay open beyond 31 August 2026 unless MCA issues a further circular. Missing it means paying the full additional fees, which for multi-year defaults can run into lakhs of rupees, plus exposure to adjudication and possible director disqualification. Treat the extra weeks as a hard cut-off, not a soft one.

Who should use CCFS-2026, and who should not?

CCFS-2026 suits any company sitting on overdue annual filings, whether a private limited company, one person company, Section 8 company or Nidhi company. It is most valuable for companies with two or more years of defaults, where the additional fee savings are largest. It is optional, so already-compliant companies need not act. A compliance health check confirms exactly which forms are pending.

The scheme is not a fit in a few situations. Companies already struck off, under liquidation, or holding a final strike-off order may not be eligible. The scheme also applies only to companies registered under the Companies Act, so limited liability partnerships and other structures follow their own separate compliance route. If prosecution has already begun, the immunity may not extend to those proceedings.

- Good fit: active companies with pending private limited company compliance, OPC annual compliance, Section 8 compliance or Nidhi company compliance.

- Not suitable: companies already struck off or under active prosecution for the same default.

Summary

CCFS-2026 now stays open until 31 August 2026, giving companies extra working days to clear overdue ROC filings at the normal fee plus only 10% of the additional fees. Inactive companies can instead move to dormant status at 50%, or strike off at 25%, of the normal fee. Confirm your pending forms early and complete your ROC annual filing before the window closes.

Frequently Asked Questions

What is the new CCFS-2026 deadline?

Why did MCA extend CCFS-2026 to 31 August 2026?

What is the Companies Compliance Facilitation Scheme, 2026?

How much do companies pay under CCFS-2026?

Which forms are covered under CCFS-2026?

Can a dormant company use CCFS-2026?

How can a company strike off under CCFS-2026?

What happens after CCFS-2026 ends on 31 August 2026?

Does CCFS-2026 give immunity from penalties?

Is CCFS-2026 mandatory for companies?

What is the late fee for ROC filing without CCFS-2026?

Which circular extended the CCFS-2026 deadline?